Euronext Lisboa

Euronext Lisboa

Índices portugueses

| Índices | Último | % |

|---|---|---|

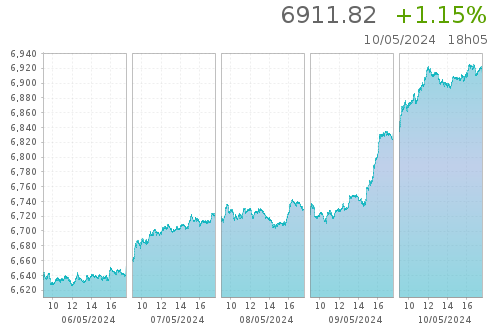

| PSI | 6 612,51 | +1,07 % |

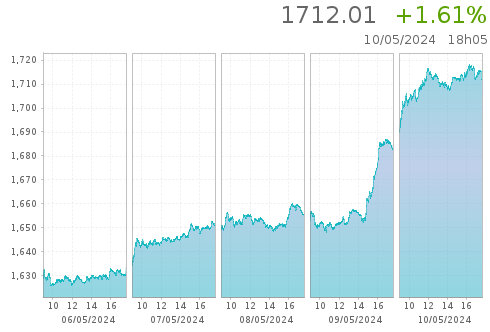

| PSI ALL-SHARE | 1 622,33 | +1,26 % |

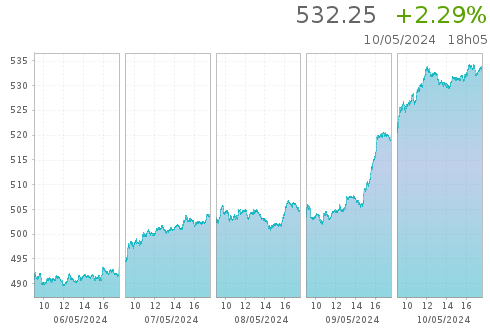

| PSI LEVERAGE | 488,279 | +2,14 % |

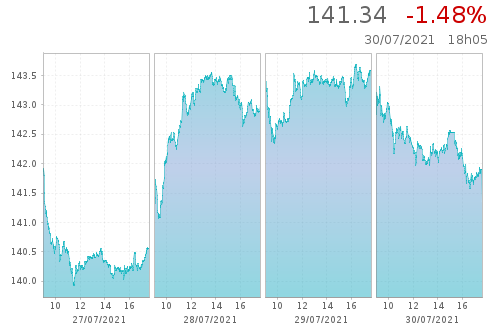

| PSI HIGH DIV NR | 141,34 | -1,48 % |

| PSI XBEAR GR | 34,199 | -2,12 % |

Índices EU

| Nome do instrumento | Último preço | Day-change-relative |

|---|---|---|

| EURONEXT 100 | 1 519,43 | +0,96 % |

| CLIMATE EUROPE | 1 923,03 | +1,17 % |

| LOW CARBON 100 | 162,97 | +1,01 % |

| NEXT BIOTECH | 2 076,89 | +0,68 % |

| ESG 80 | 2 069,75 | +1,10 % |

Câmbio

| Nome do instrumento | Último preço | Day-change-relative |

|---|---|---|

| EUR / USD | 1,07015 | -0,26 % |

| EUR / GBP | 0,85645 | -0,14 % |

| EUR / JPY | 169,14968 | +1,32 % |

| EUR / CHF | 0,97885 | +0,02 % |

| GBP / USD | 1,2488 | -0,19 % |

Indices portugueses

PSI 20

PSI ALL-SHARE

PSI High div

PSI LEVERAGE

PSI XBEAR

Mercados a contado

Comunicados empresas

MAIS SOBRE A EURONEXT LISBON

Saiba mais sobre os mercados Euronext

Visite a página sobre o mercado português e saiba mais sobre a praça de eleição para os emitentes portugueses.