Euronext Lisboa

Euronext Lisboa

Índices portugueses

| Índices | Último | % |

|---|---|---|

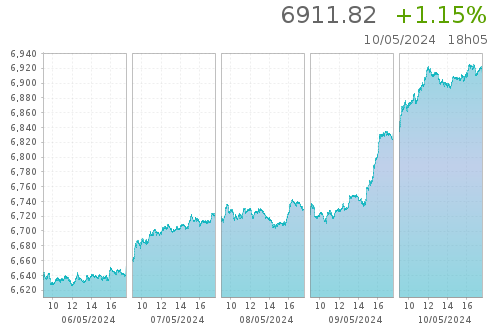

| PSI | 6 545,76 | +0,24 % |

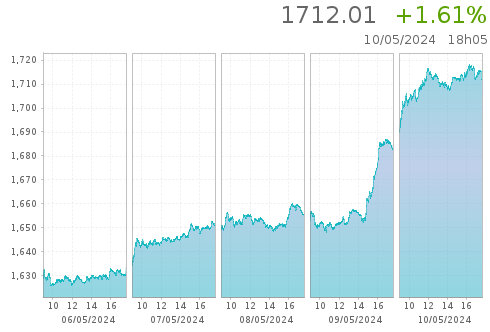

| PSI LEVERAGE | 478,578 | +0,47 % |

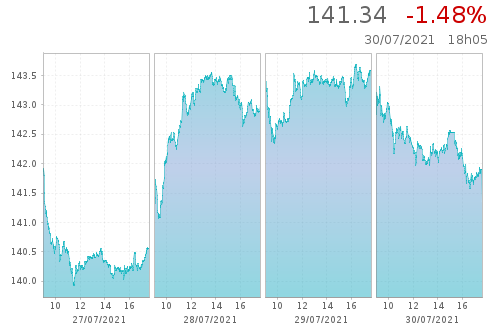

| PSI HIGH DIV NR | 141,34 | -1,48 % |

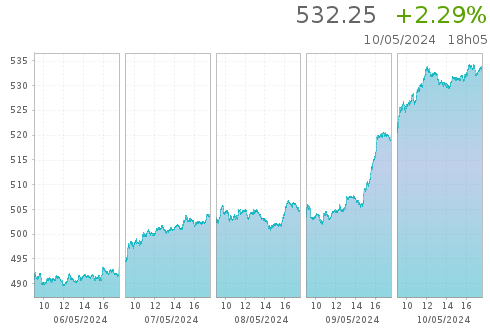

| PSI XBEAR GR | 34,901 | -0,45 % |

Índices EU

| Nome do instrumento | Último preço | Day-change-relative |

|---|---|---|

| EURONEXT 100 | 1 513,74 | -0,13 % |

| CLIMATE EUROPE | 1 909,52 | +0,15 % |

| LOW CARBON 100 | 162,13 | +0,32 % |

| NEXT BIOTECH | 2 090,86 | -0,13 % |

| ESG 80 | 2 061,76 | -0,19 % |

Câmbio

| Nome do instrumento | Último preço | Day-change-relative |

|---|---|---|

| EUR / USD | 1,07249 | +0,24 % |

| EUR / GBP | 0,85701 | -0,17 % |

| EUR / JPY | 166,9695 | +0,54 % |

| EUR / CHF | 0,9797 | +0,09 % |

| GBP / USD | 1,25144 | +0,42 % |

Indices portugueses

PSI 20

PSI ALL-SHARE

PSI High div

PSI LEVERAGE

PSI XBEAR

Mercados a contado

Comunicados empresas

MAIS SOBRE A EURONEXT LISBON

Saiba mais sobre os mercados Euronext

Visite a página sobre o mercado português e saiba mais sobre a praça de eleição para os emitentes portugueses.